What You’ll Gain From This Guide

- A realistic estimate of the cost of living in London in 2026, including monthly expenses for professionals and families.

- A clear breakdown of living expenses in London, such as rent, transport, groceries, and utilities.

- Insight into what salary is needed to live comfortably in London across different income levels.

- A simple 3-step financial framework to evaluate if relocating to London is financially manageable.

- Practical guidance on choosing the right location in London by balancing rent costs and commute time.

- An understanding of upfront relocation costs and the first 90 days of moving to London, so you can plan better.

The cost of living in London for a single professional in 2026 falls between £3,500 and £3,700 per month. In contrast, families would typically spend between £6,500 and £7,000+ monthly. The primary cost driver in living expenses in London is housing/rent.

The living expenses in London can be easily managed for a better experience with budgeting, knowing where costs can be managed, and a buck can be saved. Our guide will tell you everything you need to know about costs, salary, housing and other expenses of living in London before you move.

Is London Financially Manageable for Professionals?

While relocating to London, one of the major concerns for every professional is whether they can afford to live in one of the world’s most expensive cities. Well, rest assured, professionals can easily build a stable life in London after understanding how living expenses in London work.

Especially for mid to senior professionals, London is demanding but manageable with structured planning. It is noted that salaries across finance, technology, and other professional sectors have seen stable growth. Offering typical salaries to live comfortably in London to professionals.

It can be overwhelming to handle the cost of living in London per month at first glance, but long-term budgeting and predictable expenses are the main takeaway. The major expenses, like rent and housing, are predictable. Additionally, transport, groceries and utilities mostly remain stable once you settle in.

The predictability thus helps professionals in creating clear financial plans. Once housing, commuting, and other essential expenses and bills are easy to account for, the remaining budget is easy to allocate across lifestyle and savings.

Hence, with budgeting, living in London becomes easy for professionals once the initial phase of settling and relocating is over. It should be noted that location decisions play an important role — living outside the centre provides a better value.

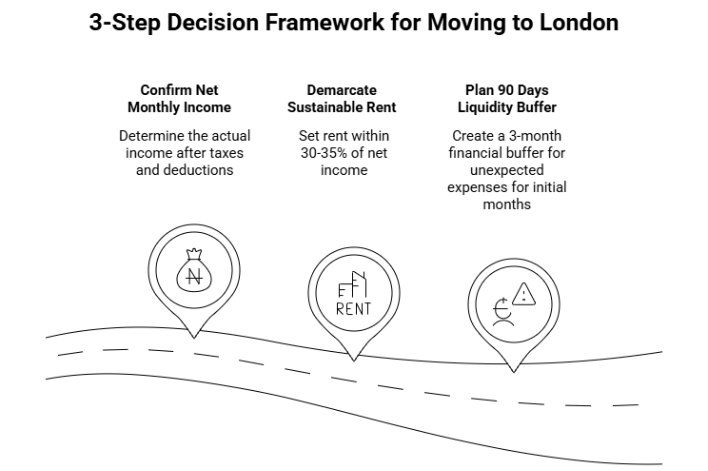

The 3-Step Decision Framework Before You Move

Now, while relocating, how to work it out to make it less overwhelming. The best way to make the move to London is to create a simple financial framework. Instead of putting a lot on your shoulders at once, the 3-step decision framework helps you to manage your London monthly expenses much better and easily.

Once the 3 steps align, it eases your transition to living in London, making it far more manageable than initially thought. The 3-step decision framework flows like so:

Step 1: Confirm the net monthly income

Start with the main number of your budget, the net monthly income that reaches your bank account after taxes and all the deductions. This key amount is the crucial salary on which the daily life in London revolves. It is better to take it monthly rather than yearly, since you will be spending it while you stay here.

The net monthly income sets a base for financial decisions for the month and the foreseeable future. Once the net income is clear, it is easier to budget everything for a stable life in London.

Step 2: Demarcate Sustainable Rent by 30–35% Rule

The largest expense, housing, always drives the average cost of living in London, making setting a rent boundary an essential step. The basic benchmark while looking for housing in London is to keep rent within 30–35% of your net income (which we concluded in the first step).

By following the rent limit, you can maintain a balance between housing, lifestyle expenses, and savings. Now, when you choose a home in London, instead of stretching your budget for a central location, choose slightly outer areas for a more sustainable financial routine.

London’s extensive transport system more than makes up for the distance you give up. The housing costs in London’s outer boroughs are much lower than in the centre, and they still keep you connected to everything with ease.

Step 3: Plan a 3-month Liquidity Buffer

Relocation expenses don’t stop at rent and deposits, as moving costs, setup, purchases, visa, and innumerable unexpected expenses can come knocking during the first few months.

To tackle unexpected expenses while relocating to London, the crucial step is to maintain a 3-month financial buffer. With the liquidity buffer in place to absorb any unexpected expenses, professionals can easily adjust to living in England’s capital. Enough time is left to establish routines and focus on work without sudden shocks of financial pressure.

What Actually Determines Financial Comfort in London

Housing alignment is the major determinant of financial comfort more than any small daily expense in London. Rent being the major expense is the single factor that determines a professional’s financial stability in London.

Therefore, the 30–35% rent-to-income rule is essential to follow to ensure financial comfort in the British capital. Staying in the range allows professionals to have enough leftover for groceries, transport, lifestyle spends, unexpected costs and savings.

After rent, the next cost is commuting predictable and easy to manage. One of the major benefits of living in London is that its public transport system is structured in fixed fare areas and can be accessed with a monthly Travelcard or Oyster card. A typical contactless card for Zones 1-3 in London costs around £201, allowing accurate budgeting for every month.

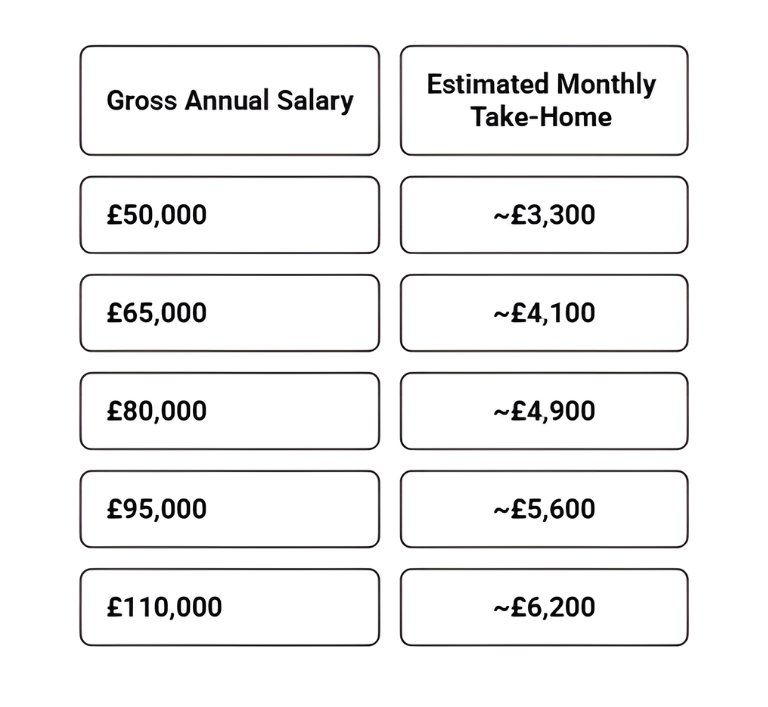

To understand how income will translate into actual financial comfort in London, let's look at monthly take-home salaries under the latest UK 2025/26 tax bands.

Taking these into account, we can estimate the salary required to live in London comfortably. Professionals who earn around £50k–£60k can live in London with budget and planning. However, it is important to choose housing outside central areas.

At £70k- £90k, financial flexibility improves significantly, and private apartments and central locations are easier, with enough left for other expenses and savings.

With an annual salary over £100k, financial pressure can be reduced a lot. Maintaining a balance between work, lifestyle, and the benefits of living in London is far easier at these levels. However, the rent-to-income ratio should be followed for the best-balanced lifestyle.

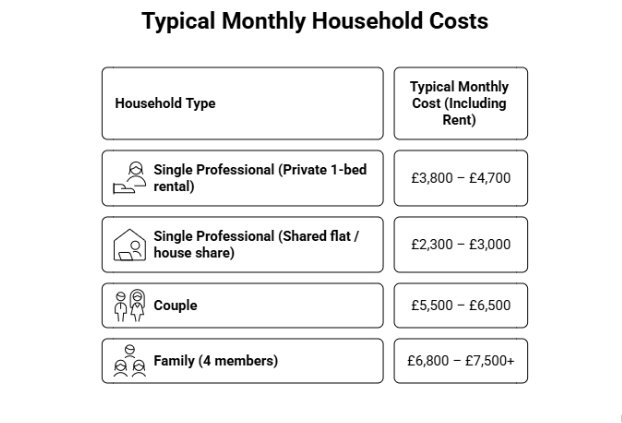

What Monthly Life in London Typically Looks Like

To understand what a monthly life in London typically looks like, let’s look at a breakdown of expenses. Rental data shows that the average rent in London is approximately £2,716 per month, making it the major expense. At the same time, other expenses, such as commuting, groceries, utilities, and other essentials, are largely predictable.

Look at the table below to appraise the cost of living in London for a single person, a couple, and a family.

Additionally, the average cost of food in London for a single professional would come to £150–£250, covering groceries. While £150–£250 would be spent on utilities, including internet and £150–£200 on public transport (depending on the commuting zones).

For single professionals, living in shared accommodation in London is a much better financial decision for a more stable and flexible budget.

These numbers are to identify typical spending patterns rather than strict budgets. Housing is a major factor affecting these expenses. For example, a person renting privately is likely to spend at the higher end of the projected range compared to someone renting in outer boroughs or living in shared accommodation.

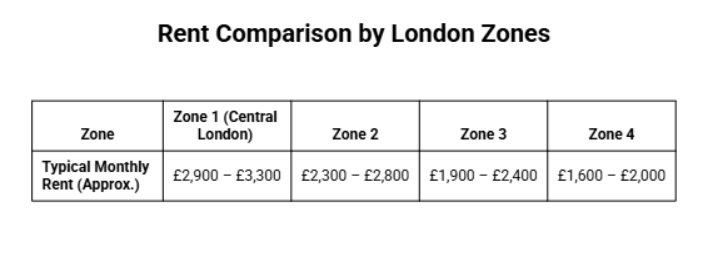

Location Decisions: Cost vs Time Trade-Off

The location you live in, London, determines two key aspects: your rent and the time and money you spend on commuting. Professionals usually face a trade-off between living in central areas at higher costs and moving to outer areas with lower rents, while accepting longer commutes.

The latest rental data across different zones in London illustrates how location is directly related to housing costs. The basic rent across London averages £2,716 per month.

The cost of living in London understandably gets affected according to your location choice. A professional will save hundreds of pounds by living in an outer zone, but will spend more time travelling each month.

Travel data suggests that many professionals tend to spend 60-70 minutes daily in commutes. When translated to an annual basis, 60-70 minutes means spending 250 hours per year on travelling rather than at home or work.

The transport costs in London also increase as zones are included. Hence, professionals need to balance between rent and travel while deciding on a location to rent while relocating to London.

On the other hand, families take proximity to schools, parks, quieter neighbourhoods, safety, and larger living spaces in housing into consideration while making a decision. Most families are known to choose outer zones because of better value and more space.

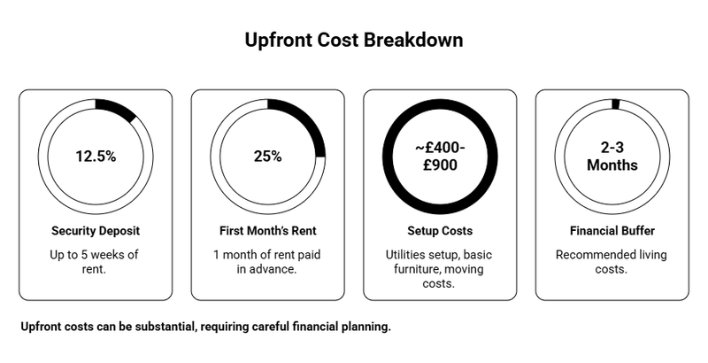

Planning Your First 90 Days: What to Expect Upfront

At the beginning of your process to relocate to the British capital, there are things that you can expect upfront in terms of expenses. Upfront costs are higher in the first month but predictable, making them manageable.

It should be noted that for a short period of time, professionals face elevated expenses, with deposits, setup costs and other things occurring at the same time.

Under the UK Tenant Fees Act, landlords can request a deposit capped at 5 weeks’ rent and holding deposits are limited to one week's rent to reserve a property. This helps keep the rental system transparent and balanced for relocating professionals.

The simplified upfront cost overview will help in planning for the initial months of the move.

What does Upfront Costs mean in Practical Terms?

Although the first month of relocation feels heavy financially, the payments are one-time only. After the initial setup is done, expenses and monthly budgets stabilise.

Many professionals who aim to reduce the initial living expenses in London are known to choose temporary or flexible housing options. Choosing temporary stays allows time to understand different neighbourhoods, commuting routes, timings and other factors before any commitment to full tenancy.

For families, the upfront costs mostly remain the same, though renting bigger apartments/housing naturally increases deposits. However, with a 3-month financial buffer and realistic expectations and planning, the first 90 days of relocation to London become a learning curve rather than an unpredictable financial burden.

Relocating Alone vs Relocating With Family

Finally, let's look closely at the difference between relocating to London alone and with a family. Cost dynamics differ depending on household structure, although the main cost drivers remain the same – housing, transport and daily expenses. These costs change depending on whether one is relocating alone or with family.

Understanding these differences while relocating or planning to do so can help a lot.

Individual Professional

- The individual professionals who are relocating to London have greater flexibility than families. They can reduce housing costs by choosing shared accommodation or smaller flats.

- Monthly spend on groceries, utilities, transport, etc, stabilises once housing is secured. Additionally, it is suggested from past data that an individual spends roughly £1,400 on expenses apart from rent.

- Professionals balance rent costs by choosing to stay in outer boroughs and commuting to business districts and offices daily.

- Solo relocation also provides enough flexibility with spending habits, such as dining, travel, or entertainment, depending on income.

Families

- Families have to face a considerably larger cost structure because housing, as well as childcare, gain importance over everything else. Hence, families require two or three bedroom apartments, which in turn increases rent as compared to one bedroom and flat shares.

- The nursery and childcare costs are the highest additional costs, with nursery costing around £238.95 for a week in London.

- The childcare estimates fall between £900 and £1800 for a month in the British capital, depending on the care requirements.

- While choosing an accommodation, families also have to factor in many things such as proximity to school, quieter settings, quick access to parks, and so on. However, these factors mostly shift families to the outer boroughs more.

- Family budgets need to be more than individual ones and must take into account extra expenses such as education, childcare, and growing household expenses over time.

Undeniably, moving to London with family involves higher costs, but they are manageable by choosing neighbourhoods in outer boroughs. The outer boroughs also have larger homes and other community amenities.

Ultimately, it comes down to how costs are balanced. Individuals prefer flexibility and commute, while families focus on childcare, space and schools, affecting housing and budget decisions.

If This Feels Overwhelming: A Practical Way to Think About It

Relocating to a major city like London can be complex and overwhelming, with so many things to consider in order to strike a balance. However, professionals soon discover that living expenses in London are fairly predictable and so easy to budget around.

In a practical way to think about it, while relocating to the British capital, professionals need to focus on three core principles rather than on every small expense.

First, income alignment is crucial. Matching the take-home income to living expenses provides financial clarity.

Second, maintaining the rent-to-income ratio is sustainable and ensures that housing does not take the entire monthly budget. When rent is within this manageable spectrum, daily expenses and savings become easier to navigate even in a global city.

Third, a short-term liquidity buffer is key and helps in absorbing any initial temporary financial pressure that is inevitable with relocation. The first few months overload professionals with deposits, setup costs, and other unpredictable costs. So it is best to have a financial buffer to absorb it without destroying the base budget.

When these three elements – income alignment, sustainable rent to income ratio, and a financial buffer are in place, the overall experience becomes far more manageable.

London may be one of the most expensive cities, but with structured planning and budgets, professionals can find financial stability.

Frequently Asked Questions

1. Is a £70,000 annual income enough to live comfortably in London?

Yes, a £70,000 annual income is generally sufficient for a single professional in London if rent follows the 30-35% rent to income rule. At this level, living in Zone 2 or 3 with moderate savings is realistic. Comfort depends primarily on housing alignment rather than day-to-day expenses. For families, however, this salary may require more careful planning, especially if childcare is involved.

2. How much does it realistically cost to live in London per month?

A single professional typically spends £2,500–£3,200 per month, while families often require £4,500 or more, depending on housing size and location. Housing usually accounts for 40–60% of total monthly costs. Once rent is defined, most other expenses, including utilities, transport, and groceries, remain relatively predictable.

3. How much money should I have saved before relocating to London?

Most professionals should plan at least £6,000–£8,000 in accessible savings before relocating. This typically covers deposit, first month’s rent, setup expenses, and initial adjustments. Families renting larger properties should prepare higher reserves. Liquidity reduces pressure and allows better long-term housing decisions during the first 90 days.

4. Is it better to rent long-term immediately or choose short-term housing first?

Short-term housing is often safer initially. Many relocating professionals prefer flexible accommodation for the first 1–3 months to assess commute times, neighbourhood suitability, and lifestyle preferences before signing a 12-month lease. This approach reduces the risk of costly relocation adjustments later.

5. What salary allows you to save £1,000 per month in London?

Typically, savings of £1,000 per month become realistic at £85,000–£90,000+ annual income, assuming disciplined housing costs. Savings potential depends more on rent selection than income alone. High earners who overspend on housing often experience less flexibility than moderate earners who plan strategically.

6. Can a family live comfortably on £100,000 in London?

Yes, a household income of £100,000 can support a comfortable living in Zones 2–3 if rent remains proportionate. However, childcare, property size, and school proximity significantly influence flexibility. Strategic housing selection is critical to maintaining savings and long-term financial comfort.

7. What is the biggest financial mistake professionals make when moving to London?

The most common mistake is committing to an expensive long-term lease too quickly. Housing decisions made under time pressure often lead to unnecessary financial strain. Aligning rent with income and allowing a short adjustment period typically produces a more stable first year.

8. Is London financially worth relocating to for work?

Yes, London can be financially worthwhile at mid-to-senior income levels due to strong career progression and long-term earning potential. However, sustainability depends on structured housing decisions and realistic cost planning. With proper alignment, the city becomes predictable rather than overwhelming.